Yield curve |

您所在的位置:网站首页 › bootstrapping spot rates › Yield curve |

Yield curve

|

The formula below shows the basic relationship between short and long-term interest rates

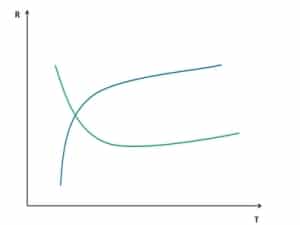

Note that long-term interest rates are a geometric average of the short-term interest rates. As a consequence, changes in short-term interest rates will only have a limited impact on long-term interest rates. As a result, long-term interest rates are much more stable than short-term rates. Forward rateUsing the implications of the ‘pure expectations’ theory, we can calculate forward interest rates that can be used for discounting cash flows. Forward interest rates are simply future short-term interest rates that the market expects. We can determine this expected interest rate for investing money for one year, at the start of next year (r1,2) by using the interest rates we observe today. Today, we know the current 1-year short-term interest rate r0,1, as well as the current 2-year interest rate r0,2. We don’t observe r1,2, but we can infer it from the observed rates using the formula

|

In practice, the yield curve is almost always upward sloping. This means that long-term interest rates are generally higher than short-term rates most of the time. Therefore, short and long-term interest rates are not perfect substitutes. This is probably because different investors have a preference for different investment horizons when investing. However, as investing for longer periods of time means that the investor cannot withdraw his money for quite some time. He or she requires an additional compensation for long-term investments.

In practice, the yield curve is almost always upward sloping. This means that long-term interest rates are generally higher than short-term rates most of the time. Therefore, short and long-term interest rates are not perfect substitutes. This is probably because different investors have a preference for different investment horizons when investing. However, as investing for longer periods of time means that the investor cannot withdraw his money for quite some time. He or she requires an additional compensation for long-term investments.

【本文地址】